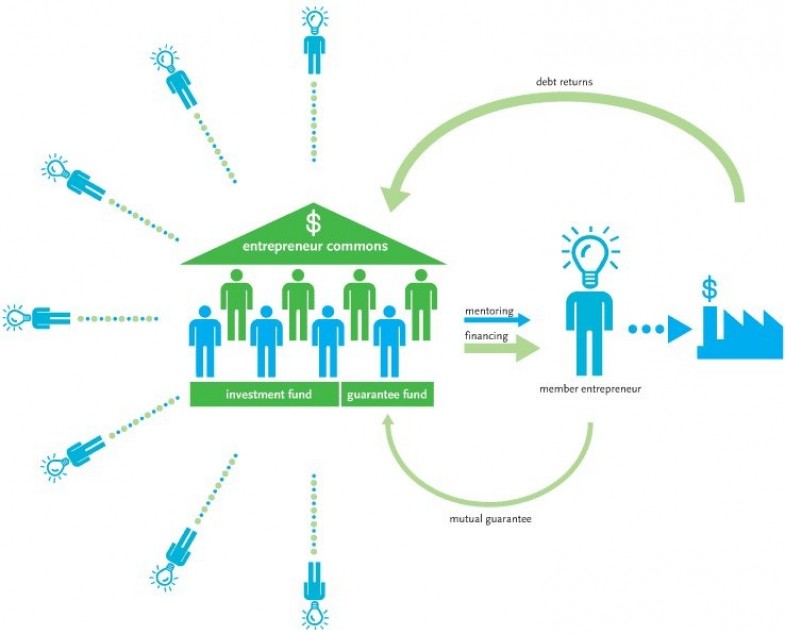

The Entrepreneur Commons is trying to change the process of financing startups, by doing loans instead of equity deals. The concept is similar to what is being done in Microfinance, but applied to entrepreneurs in developed countries rather than the poor in developing countries.

After looking at Venture Capitol funds (VC’s), and after managing the European American Angel Club for 2 years now, I have come to the conclusion that entrepreneurs are not really being served properly when it comes to seed funding. And I would like therefore to propose the concept of an Entrepreneur Commons to help with the issue.

I have seen are roughly 3 types of angels:

- The super-angel, who has enough money to be a one-man show VC playing with his own money (and maybe money from a few friends). Either he is known by the VC community, and he is treated well by them because he can source good deals for the later-stage rounds, or he has enough money within his ecosystem that he can help entrepreneurs all the way through.

- The social type, who has money and like toying with the idea that he could invest and may do so one day. He likes attending meetings and talking about it, but the reality is that he never really invests in anything.

- And then you have everybody else in between these 2 types.

This last group of angels faces a lot of issues with the model as it is today:

- Angels their put money down and they have no clue when it will come back (if ever). Typical time before a cash event is 7 to 9 years if you believe angels who have done it for a while

- When investing in early stage, they have no real data to figure out a valuation, so any equity deal is based on arbitrary valuations where somebody is getting a bad deal on one side (angel) or the other (entrepreneur)

- If the business requires additional funding, Angels are being squeezed of the deals by VCs, who impose liquidation-preference clause

- And finally because you are just an Angel after all and not a fund, you are limited in your resources and cannot really spread yourself into a number of deals that is statistically relevant.

So in the end, they are playing the lottery, and they know it. And because they are playing the lottery, they want the reward to be as big as possible if they win, so they tend to shoot for companies with a potential for return of at least 10x the investment.

From the entrepreneur side, this leaves out of the system a whole lot of very good startups with very promising businesses but not “hot” enough. This is even more critical these days when you see an emergence of “social entrepreneurs” who are interested in making money, but whose focus (and measure of success) is also to help the community one way or another. They are not really non-profit, so most of the time they do not qualify for grants, but they are not the 10x type either. Meanwhile they clearly deserve help.

The way I see out of this situation is the Entrepreneur Commons:

A not-for-profit social network of entrepreneurs providing financing for early stage company through debt guaranteed by a mutual guarantee fund. The financial risk is mitigated by the mutual guarantee fund. The risk on the “management” side is mitigated by the social network: loans are by invitation only, so you will have to be approved by your peers to get in. And the typical scalability issue faced by general partners in a VC fund (which causes the famous “funding gap”) is also resolved by the social network: the size of loans and the number of entrepreneurs involved is no longer a problem, and if anything it helps stabilize the results of the group as a whole.

The project is starting to get some traction, and we have been getting a lot of positive feedback – the recent post from my friend Jessica is a good example of the reactions I get.

The goal is now to confirm the blueprint for this model, so that it can be replicated anywhere. We have started looking for funds so that we can make loans soon. Stay tuned…